Introduction

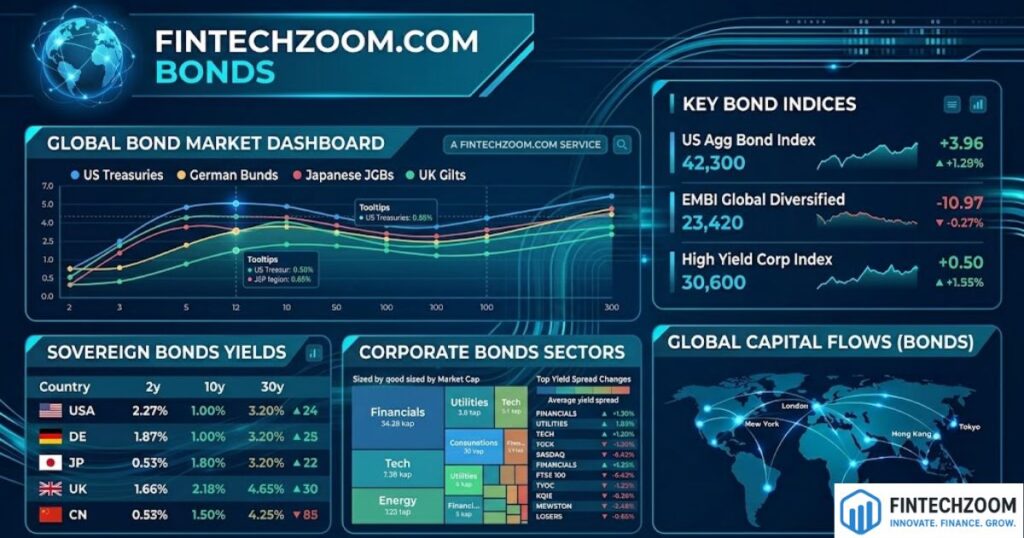

Navigating the fixed-income market requires a solid understanding of macroeconomics, interest rate cycles, and risk management. For decades, institutional investors used debt instruments to preserve capital and generate reliable income streams. Today, retail investors are increasingly entering this space to protect their portfolios from stock market volatility and economic uncertainty. Tracking these shifting dynamics requires access to accurate data, real-time yield curves, and expert market analysis. The dedicated financial tracking tools at fintechzoom.com bonds offer a structured environment where investors can monitor global debt securities, corporate issuances, and central bank policies.

As central banks adjust monetary policies to combat inflation or stimulate growth, bond yields react instantly, creating ripple effects across the entire financial system. Understanding how these price movements affect your broader investment portfolio is crucial for long-term financial success. Whether you are looking into stable government securities or exploring higher-yield corporate debt, having a centralized dashboard simplifies the research process. This article breaks down the mechanics of the fixed-income sector, helping you interpret key yield metrics and build a balanced investment strategy.

Understanding Fixed-Income Asset Classes

The Fundamentals of Fixed-Income Security Pricing

Fixed-income securities function fundamentally as loans made by an investor to a borrower. The borrower, which could be a government entity or a corporation, agrees to pay back the principal amount on a specific maturity date. In exchange for the upfront capital, the issuer makes regular interest payments, known as coupon payments, to the lender. The pricing of these instruments on the secondary market fluctuates constantly based on prevailing economic conditions and broader market sentiment.

A critical concept for every investor to master is the inverse relationship between debt security prices and interest rates. When central banks raise benchmark interest rates, newly issued debt instruments offer higher coupon rates to attract investors. Consequently, existing instruments with lower coupon rates become less attractive, causing their secondary market prices to drop. Conversely, when interest rates decline, older, higher-yielding instruments increase in market value. Recognizing this pricing dynamic is essential for managing capital gains and losses within a fixed-income portfolio.

Deciphering the Importance of the Yield Curve

The yield curve is one of the most powerful predictive metrics in macroeconomics, representing the relationship between interest rates and varying maturity dates. Typically, a healthy economy features a normal upward-sloping curve, meaning long-term debt instruments pay higher yields than short-term ones. This premium compensates investors for locking up their capital over extended periods, where inflation and economic changes present greater risks. Analysts track this curve closely to forecast shifts in economic momentum.

An inverted yield curve occurs when short-term yields surpass long-term yields, signalizing that investors expect economic growth to slow down significantly in the future. Historically, a persistent inversion has often served as a reliable warning sign of an impending economic recession. When tracking fixed-income dashboards, paying close attention to the gap between short-term notes and long-term bonds helps investors adjust their risk exposure. Monitoring these structural shifts allows market participants to shift capital into safer, more resilient assets before broader market corrections occur.

Government Debt and Sovereign Risk Profiles

Government debt securities, particularly those issued by major global economies, are widely considered the bedrock of the global financial system. Because these instruments are backed by the taxing power and currency-printing authority of sovereign nations, the risk of default is virtually non-existent for top-tier issuers. Consequently, the yields on these government securities serve as the benchmark risk-free rate against which all other financial assets are measured and priced.

However, sovereign risk profiles vary significantly across different geographic regions. Emerging market government debt often carries substantially higher yields to compensate investors for currency fluctuations, political instability, and lower fiscal transparency. When building a global investment strategy, balancing domestic treasury security stability with the growth potential of foreign sovereign debt requires careful analysis. Tracking credit ratings from major agency bureaus provides a standardized method for evaluating the underlying creditworthiness of various sovereign issuers worldwide.

Evaluating Corporate Debt and Credit Spreads

Corporate debt instruments allow private enterprises to raise substantial capital for expansion, research, or restructuring without diluting existing shareholder equity. Unlike government securities, corporate issuances carry varying degrees of default risk, meaning the enterprise might fail to meet its payment obligations. To account for this risk, corporations must offer higher interest rates than government entities, creating a metric known to analysts as the credit spread.

Credit rating agencies evaluate corporate issuers and assign scores ranging from prime investment-grade down to speculative junk status. Investment-grade corporate debt offers a comfortable middle ground for conservative portfolios, providing higher returns than treasuries while maintaining a strong probability of full repayment. Speculative or high-yield instruments carry elevated risk but offer substantial coupon payments that attract aggressive income seekers. Tracking changes in corporate spreads helps investors determine whether the market is pricing corporate risk optimistically or conservatively.

Inflationary Pressures and Fixed-Income Returns

Inflation is the primary enemy of fixed-income investing, as it steadily erodes the purchasing power of fixed interest payments over time. If an investor holds an asset paying a fixed three percent annual coupon while consumer prices rise by four percent, the investor experiences a negative real return. Because of this vulnerability, inflation expectations play a massive role in shaping daily market pricing and yield demands.

To protect against this erosion, financial markets offer inflation-indexed securities, such as Treasury Inflation-Protected Securities. The principal value of these specialized instruments adjusts automatically in response to changes in consumer price indices, ensuring that the investor’s real purchasing power remains intact upon maturity. When inflation indicators surprise the market on the high side, traditional fixed-coupon instruments typically experience selling pressure, while inflation-protected assets see increased capital inflows from protective investors.

Portfolio Diversification Using Debt Instruments

A primary reason individual investors add debt securities to their portfolios is to achieve effective diversification and smooth out overall returns. Historically, equities and fixed-income assets often move in opposite directions during market cycles, providing a cushion when stock markets experience corrections. During periods of corporate earnings declines or geopolitical tension, capital frequently flees volatile equity markets and seeks refuge in the stability of debt instruments.

This flight-to-safety phenomenon helps prevent severe drawdowns in balanced portfolios, allowing investors to maintain long-term financial stability. The specific allocation of debt instruments within a portfolio depends heavily on an individual’s age, retirement timeline, and personal risk tolerance. Younger investors might maintain a minimal allocation focused on high-growth equities, while individuals approaching retirement often increase their fixed-income exposure to lock in reliable cash flow and protect their accumulated wealth.

The Digital Transformation of Bond Trading Platforms

The fixed-income market was traditionally dominated by institutional desks trading massive blocks of debt over institutional phone networks and private terminals. This lack of transparency and high minimum investment requirements kept individual retail investors on the sidelines for generations. However, the digital transformation of financial technology has revolutionized how these instruments are bought, sold, and analyzed by the public.

Modern financial portals and electronic trading platforms have introduced greater price transparency, lower transaction fees, and fractional investing capabilities. Individual traders can now scan real-time ask and bid prices, compare yields across hundreds of issuers simultaneously, and execute trades digitally. This increase in accessibility allows independent investors to construct highly customized income portfolios with the same precision and data depth that was once exclusive to large-scale asset management firms.

FAQs

What is the difference between a bond’s coupon rate and its current yield? The coupon rate is the fixed annual interest percentage set when the bond is originally issued, calculated based on its par value. The current yield is a dynamic calculation determined by dividing the annual coupon payment by the asset’s current fluctuating secondary market price.

How does maturity duration affect an investment’s risk profile? Maturity duration measures how sensitive a debt instrument’s price is to changes in interest rates. Long-term instruments have higher duration, meaning their secondary market prices fluctuate much more dramatically when interest rates move compared to short-term notes or bills.

Are the interest payments received from municipal bonds taxable? In many jurisdictions, interest earned from municipal bonds issued by local, city, or state governments is exempt from federal income taxes. In some cases, if the investor resides in the municipality issuing the debt, the income may also be exempt from state and local taxes.

What happens if a corporate bond issuer goes bankrupt? If a corporation enters liquidation, bondholders hold a senior claim on the company’s remaining assets compared to preferred and common stockholders. Secure debt holders are paid first from asset sales, followed by unsecured creditors, while equity shareholders typically face total capital loss.

Conclusion

Building a resilient financial portfolio requires a sophisticated understanding of how fixed-income markets operate and interact with the broader economy. While stock markets often capture public headlines with dramatic price swings, the global debt market serves as the underlying engine driving corporate expansion and government fiscal policy. Utilizing tracking dashboards like fintechzoom.com bonds provides individual investors with the tools necessary to analyze yield movements, monitor credit spreads, and track shifting macroeconomic trends efficiently.

Achieving consistent success in fixed-income investing relies on maintaining a clear view of inflation trends, central bank rate decisions, and credit risk profiles. By learning to read the yield curve and understanding the inverse relationship between asset prices and interest rates, you can position your capital strategically across different economic cycles. Whether your goal is to safeguard accumulated wealth from equity market volatility or secure a predictable stream of retirement income, debt securities offer versatile solutions. Incorporating consistent research methods, diversifying across distinct asset classes, and leveraging modern digital analytics tools will allow you to navigate the complexities of fixed-income markets with confidence.